In January 2022, The Ministry of Finance announced that the UAE government will be implementing Federal Corporate Tax (CT) on the net profit of businesses. The Corporate Tax in UAE came effective from the 1st of June 2023. Corporate Tax or Corporate Income Tax or Business Profits Tax will be applicable on or after the 1st of June 2023 depending on the financial year followed by the businesses, and from there on, all over the country, every business apart from the exempted group will be subjected to CT. Corporate tax is a type of direct tax imposed on net income. At present, the UAE has recorded the lowest tax rate of 9%compared to other GCC countries. On recalling the G7 countries’ meeting in 2021, the Gulf countries entered into an agreement where a global minimum corporate tax return of 15% was introduced. The United Arab Emirates chose 9% over 15% to reduce its direct impact on entrepreneurs. Business entities are the ones subjected to this direct tax, while individuals’ earning income in their personal capacity, which does not require a commercial license, is not taxable.

In January 2022, The Ministry of Finance announced that the UAE government will be implementing Federal Corporate Tax (CT) on the net profit of businesses. The Corporate Tax in UAE came effective from the 1st of June 2023. Corporate Tax or Corporate Income Tax or Business Profits Tax will be applicable on or after the 1st of June 2023 depending on the financial year followed by the businesses, and from there on, all over the country, every business apart from the exempted group will be subjected to CT. Corporate tax is a type of direct tax imposed on net income. At present, the UAE has recorded the lowest tax rate of 9%compared to other GCC countries. On recalling the G7 countries’ meeting in 2021, the Gulf countries entered into an agreement where a global minimum corporate tax return of 15% was introduced. The United Arab Emirates chose 9% over 15% to reduce its direct impact on entrepreneurs. Business entities are the ones subjected to this direct tax, while individuals’ earning income in their personal capacity, which does not require a commercial license, is not taxable.

Registering, Filing And Paying Corporate Tax

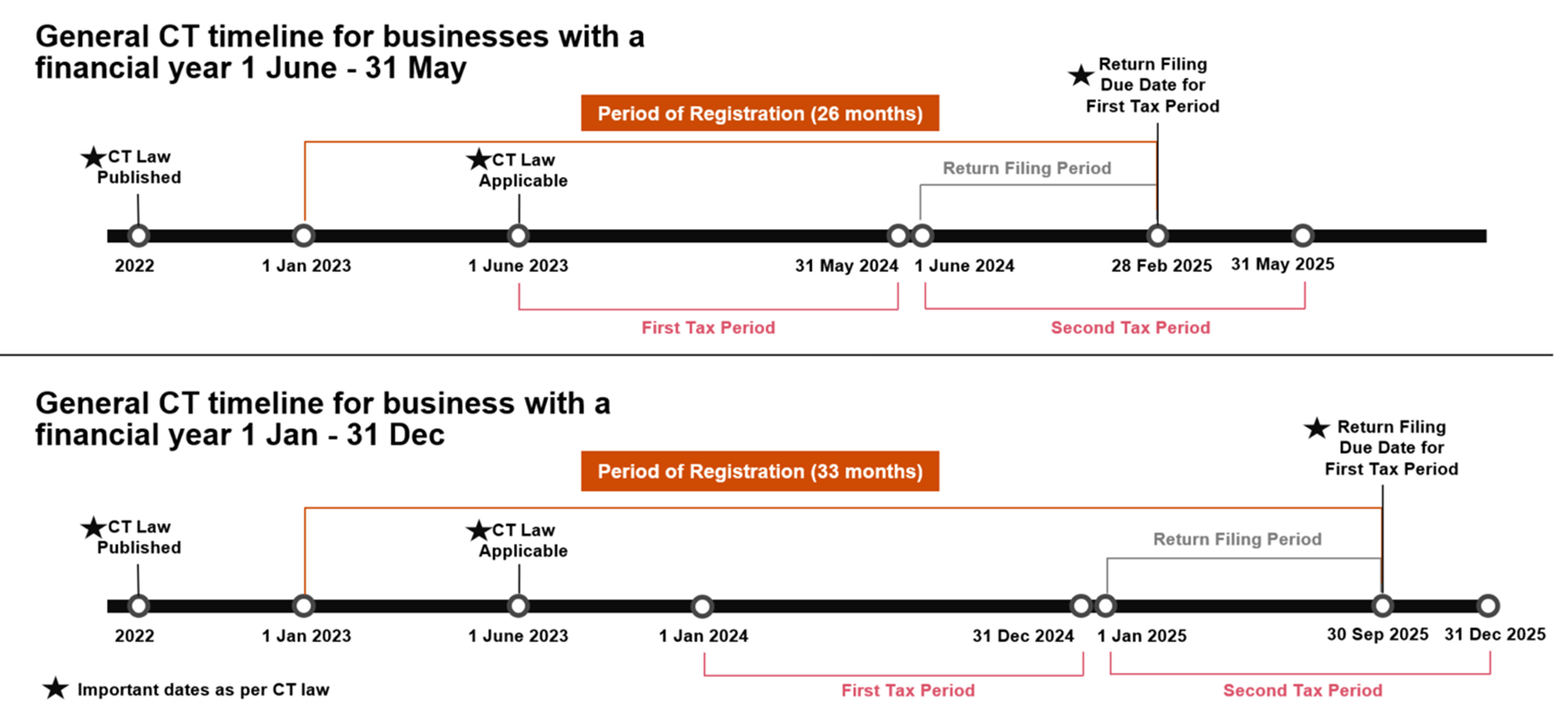

All Taxable Persons (including Free Zone Persons) will be required to register for Corporate Tax and obtain a Corporate Tax Registration Number. The Federal Tax Authority may also request certain Exempt Persons to register for Corporate Tax.

Taxable Persons are required to file a Corporate Tax return for each Tax Period within 9 months from the end of the relevant period. The same deadline would generally apply for the payment of any Corporate Tax due in respect of the Tax Period for which a return is filed.

Illustrated below are examples of the registration, filing and payment deadlines associated for Taxable Persons with a Tax Period (Financial Year) ending on 31 May or 31 December (respectively).

OJO team understand every SME or corporates has its own unique needs. Hence we offer customized services that focus on those needs, ensuring you navigate VAT requirements easily. Whether you’re seeking VAT Services in Dubai, Abu Dhabi, or across the UAE, we will work closely with you and provide guidance through the VAT registration and submission process, making sure everything remains compliant with local regulations.

OJO team understand every SME or corporates has its own unique needs. Hence we offer customized services that focus on those needs, ensuring you navigate VAT requirements easily. Whether you’re seeking VAT Services in Dubai, Abu Dhabi, or across the UAE, we will work closely with you and provide guidance through the VAT registration and submission process, making sure everything remains compliant with local regulations.

UAE VAT Registration

If you are a business owner in UAE you need to get your business registered under the VAT law that has come on effect from 1st January 2018. Once a company is registered for VAT in Dubai, it must file VAT returns on a regular basis or as set by the authority.

VAT Registration is mandatory for companies and individuals doing businesses in the UAE if the annual turnover is more than AED 375,000/-

The VAT registration processes in Dubai involve:

- Register for VAT

- Charge VAT on the invoices issued to the clienteles

- Announce the VAT to the Federal tax authorities through a VAT filing

The Importance Of VAT Registration

Experts observe that the introduction of VAT in UAE will bring long-term benefits to the country’s economy and business owners. The significant reasons why VAT registration in Dubai is considered important include:

- It enhances the business profile

- It avoids unnecessary penalties

- It allows claiming VAT refunds

- It widens the market possibilities

Documents Required For VAT Registration In Dubai

- Passport copy or Emirates ID to prove the identity of the authorized party

- Trade license copy of the company

- Certificate of Incorporation of the company

- Certificate of Articles of Association of the company

- Certificate of Power of Attorney of the company

- Description of business activities

- Turnover for the last 12 months in AED

- Supporting document for 12-month sales

- Expected turnover in the next 30 days

- Estimated value of imports for one year from all GCC countries

- Estimated value of exports for one year to all GCC countries

- Your consent whether you deal with GCC suppliers or customers

- Supporting documents for customs registration in the Emirates if applicable.

- Details of Bank Account

OJO team provides attestation services for all kinds of documents. The purpose of this procedure is to check the validity of stamp and signature on such documents, whether issued inside or outside Country. This covers attestation services provided in UAE as well as UAE missions abroad to include the legalization process of ordinary certificates issued inside and outside UAE. This encompasses educational and medical certificates, marriage and divorces contracts, powers of attorney, etc., in addition to the attestation service of commercial contracts and agreements.

OJO team provides attestation services for all kinds of documents. The purpose of this procedure is to check the validity of stamp and signature on such documents, whether issued inside or outside Country. This covers attestation services provided in UAE as well as UAE missions abroad to include the legalization process of ordinary certificates issued inside and outside UAE. This encompasses educational and medical certificates, marriage and divorces contracts, powers of attorney, etc., in addition to the attestation service of commercial contracts and agreements.

Company liquidation is a long and tedious process. It might be compulsory or voluntary. Once you plan to close down your business the government entities should be notified of the same so as to avoid any accumulated fines and penalties. License cancellation is one of the primary steps in the liquidation process and the formalities differ based on the form of company and the jurisdiction where the company is registered.

Company liquidation is a long and tedious process. It might be compulsory or voluntary. Once you plan to close down your business the government entities should be notified of the same so as to avoid any accumulated fines and penalties. License cancellation is one of the primary steps in the liquidation process and the formalities differ based on the form of company and the jurisdiction where the company is registered.

Various clearances are to be acquired from various departments such as:

- Ministry of Human Resources and Emiratisation

- Directorate of Residency and Foreigners Affairs

- The relevant Water and Electricity Authority

- The leasing entity

- FTA

Our liquidation experts provide clients with a straight-forward and cost-effective process that brings the company to an orderly end while providing formal closure and certainty to the affairs of the company. Services include from preparation of liquidation plan to appropriate documentation for company strike-off. Our deep understanding of local requirements helps us adapt and implement global best practices locally, ensuring excellent standards in all our services.